The landscape for crypto in 401k executive order investing is undergoing a fundamental shift. In August 2025, President Donald Trump signed an executive order titled "Democratizing Access for 401(k) Investors, " instructing the Department of Labor (DOL) and Securities and Exchange Commission (SEC) to facilitate access to alternative assets, including cryptocurrencies, within defined-contribution retirement plans. This directive is not merely symbolic; it marks a regulatory inflection point that could change the way Americans save for retirement.

What the Executive Order Means for Crypto in 401(k)s

The executive order, as outlined on the White House and related legal analyses, directs federal agencies to revise existing regulations, effectively opening the door for plan sponsors to add digital assets like Bitcoin and Ethereum to their investment menus. The DOL's subsequent rescission of its 2022 guidance, which previously warned fiduciaries to exercise "extreme care" before including crypto, signals a new, neutral regulatory posture. Fiduciaries are no longer discouraged from adding crypto but must still adhere to ERISA's core standard: acting prudently and in the best interest of plan participants.

This means investors may soon see cryptocurrency options appearing alongside traditional mutual funds and ETFs within their retirement accounts. However, fiduciaries are still required to thoroughly evaluate volatility, liquidity, custody risks, and suitability before offering these assets. The result is a more democratized access model, but with robust due diligence requirements remaining firmly in place.

Current Market Data: Bitcoin Holds Above $124,000

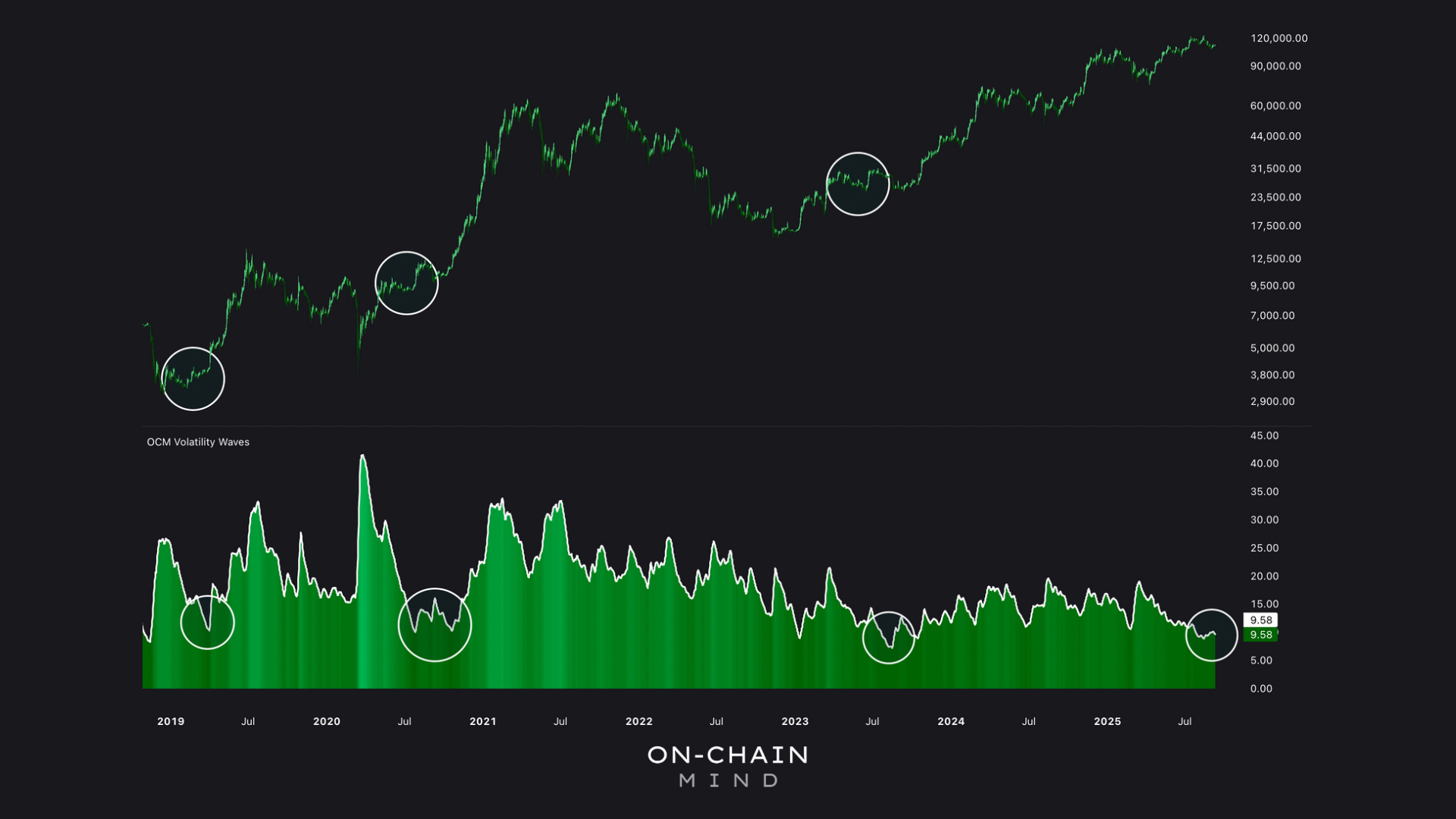

As of October 7,2025, Bitcoin (BTC) is trading at $124,266, up $424 (0.34%) over the past 24 hours. Ethereum (ETH) stands at $4,687 with a daily gain of $153.04 (3.38%). These figures underscore both the maturity and volatility inherent in digital asset markets, factors that plan sponsors must weigh when considering whether crypto belongs in a long-term retirement portfolio.

The timing of this policy shift is notable. Crypto markets have recently stabilized after years of pronounced swings; however, they remain highly sensitive to macroeconomic news and regulatory changes. For investors considering crypto allocations in their 401(k)s under this new regime, it’s essential to stay informed on price trends and risk metrics.

Fiduciary Duty Remains Paramount Under ERISA

The DOL’s updated stance clarifies that while it no longer discourages crypto as an asset class within defined-contribution plans, fiduciary standards have not been relaxed. Plan sponsors must document their decision-making process, evaluating everything from volatility exposure to custody solutions, in line with ERISA’s prudence requirements.

This means that even as regulatory barriers fall away thanks to presidential action and agency rulemaking, not every employer will rush to offer Bitcoin or Ethereum overnight. Expect early adopters among large plans with sophisticated investment committees first; smaller employers may follow as best practices emerge.

Bitcoin (BTC) Price Prediction 2026-2031: Impact of 401(k) Executive Order and Market Trends

Forecasts based on expanded 401(k) access, regulatory shifts, and evolving crypto market dynamics

| Year | Minimum Price | Average Price | Maximum Price | Year-over-Year Change (%) | Key Market Scenario |

|---|---|---|---|---|---|

| 2026 | $95,000 | $130,000 | $170,000 | -23% to +37% | Initial volatility as 401(k) adoption grows; possible corrections after 2025 highs |

| 2027 | $110,000 | $145,000 | $195,000 | +12% to +15% | 401(k) inflows stabilize, institutions increase allocations |

| 2028 | $120,000 | $165,000 | $225,000 | +14% to +15% | Mainstream adoption in retirement accounts; improved regulatory clarity |

| 2029 | $135,000 | $185,000 | $260,000 | +12% to +16% | Bitcoin halves in 2028; supply shock and demand increase |

| 2030 | $150,000 | $210,000 | $295,000 | +13% to +15% | Further institutionalization; ETFs and pension funds expand BTC exposure |

| 2031 | $165,000 | $240,000 | $340,000 | +14% to +15% | Global adoption accelerates; BTC as digital gold for retirement |

Price Prediction Summary

Bitcoin's price outlook for 2026-2031 is influenced by the historic executive order allowing crypto access in 401(k) plans. The initial years may see heightened volatility as retirement plan allocations and regulatory frameworks evolve. Over time, increased institutional participation, regulatory clarity, and Bitcoin's scarcity (post-halving) are expected to drive steady price appreciation. However, risks of corrections and high volatility remain. Investors should monitor regulatory and macroeconomic developments closely.

Key Factors Affecting Bitcoin Price

- Impact of 2025 executive order enabling 401(k) crypto investments

- Ongoing regulatory clarity and SEC/DOL guidance for retirement plans

- Market cycles, including the 2028 Bitcoin halving event

- Adoption rates among institutions and retail investors in retirement accounts

- Technological improvements (scalability, security, integration)

- Competition from other digital assets and macroeconomic trends

- Potential for corrections after rapid price appreciation

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis. Actual prices may vary significantly due to market volatility, regulatory changes, and other factors. Always do your own research before making investment decisions.

Key Questions Investors Should Ask Now

- What percentage of my portfolio should be allocated to cryptocurrencies?

- How does my risk tolerance align with crypto’s historical volatility?

- What safeguards are in place regarding custody and fraud prevention?

- How will fees compare versus traditional index funds?

- Does my plan sponsor provide education or tools specific to digital assets?

If you’re interested in deeper analysis or actionable strategies as this policy unfolds, including how allocations might be structured, see our detailed breakdown at how Trump’s executive order could reshape crypto allocations in 401(k) retirement plans.

Plan participants must recognize that, while the executive order has cleared a regulatory path, the practical implementation of crypto in 401(k)s will be gradual and nuanced. Plan sponsors and recordkeepers are likely to roll out pilot programs first, focusing on limited allocations (often capped at 5% or less) and offering only a select few digital assets, most commonly Bitcoin and Ethereum. This conservative approach reflects both fiduciary caution and the evolving nature of digital asset custody, valuation, and compliance frameworks.

![]()

For investors eager to participate, it’s important to understand that crypto exposure within a 401(k) will not mirror the unfettered access available through retail exchanges. Instead, expect curated investment menus, robust risk disclosures, and possibly even mandatory educational modules before you can allocate funds to digital assets. These safeguards are designed to address the unique challenges of cryptocurrency investing, such as price volatility, cybersecurity threats, and evolving tax reporting obligations.

How Crypto Allocations Could Impact Retirement Outcomes

The potential for outsized returns is what draws many investors to cryptocurrencies. However, historical data shows that significant drawdowns are just as common as meteoric rallies. For example, Bitcoin’s current price of $124,266 reflects remarkable growth over the past decade but also masks periods where prices fell by more than 50% in short spans. Prudent portfolio construction, balancing crypto with traditional equities and bonds, remains essential for long-term retirement security.

Pros and Cons of Crypto in 401(k) Plans

- Pro: Potential for High Returns — Cryptocurrencies like Bitcoin (BTC) have historically delivered significant gains, with BTC currently trading at $124,266. This growth potential could help boost long-term retirement savings for investors willing to accept higher risk.

- Pro: Increased Diversification — Including crypto assets in a 401(k) can diversify portfolios beyond traditional stocks and bonds, potentially reducing overall risk through exposure to alternative asset classes.

- Pro: Democratized Access — The executive order aims to make alternative assets, including cryptocurrencies, accessible to more Americans through their 401(k) plans, leveling the playing field with institutional investors.

- Con: High Volatility — Cryptocurrencies are known for extreme price swings. For example, Bitcoin’s 24-hour price ranged from $123,373 to $126,157 on October 7, 2025, underscoring the risk of significant short-term losses in retirement accounts.

- Con: Regulatory Uncertainty — Although the Department of Labor and SEC have relaxed restrictions, future regulations could change, potentially impacting the availability or treatment of crypto assets in 401(k) plans.

- Con: Fiduciary Responsibility and Complexity — Plan sponsors must thoroughly vet cryptocurrencies for suitability under ERISA rules, which adds complexity and could limit options if fiduciaries deem them too risky.

It’s also worth noting that while this executive order increases access to alternative assets, it does not guarantee performance or eliminate risk. Investors should approach these new options with clear-eyed realism: diversification can enhance returns but may also introduce new sources of volatility.

What Comes Next? Regulatory Monitoring and Investor Education

The SEC’s mandate to “facilitate access” will likely result in ongoing rulemaking around disclosures, reporting standards, and permissible crypto products within retirement plans. Expect further guidance clarifying which types of tokens qualify as eligible investments, and how plan sponsors should vet them for compliance with ERISA standards.

This regulatory evolution underscores the importance of investor education. Plan participants should take advantage of any resources offered by their employers or plan administrators, including webinars, whitepapers, or interactive tools, to make informed choices about allocating retirement funds into crypto assets.

Action Steps for Forward-Thinking Investors

- Monitor your employer’s communications about new investment options or pilot programs related to digital assets.

- Request detailed documentation on fees, risks, and custody arrangements before allocating funds to any crypto option.

- Consult with a fiduciary financial advisor who understands both traditional portfolio theory and digital asset markets.

- Stay up-to-date on regulatory changes, as further SEC/DOL guidance could impact available products or allocation limits.

- Leverage education resources provided by your plan sponsor or trusted independent sources focused on cryptocurrency retirement accounts regulation.

The landscape for crypto in 401k legal changes is evolving rapidly. As fiduciaries adapt their offerings and regulators clarify best practices, proactive investors who educate themselves, and approach these new opportunities with discipline, will be best positioned to benefit from this historic policy shift while managing downside risks effectively.

No comments yet. Be the first to share your thoughts!