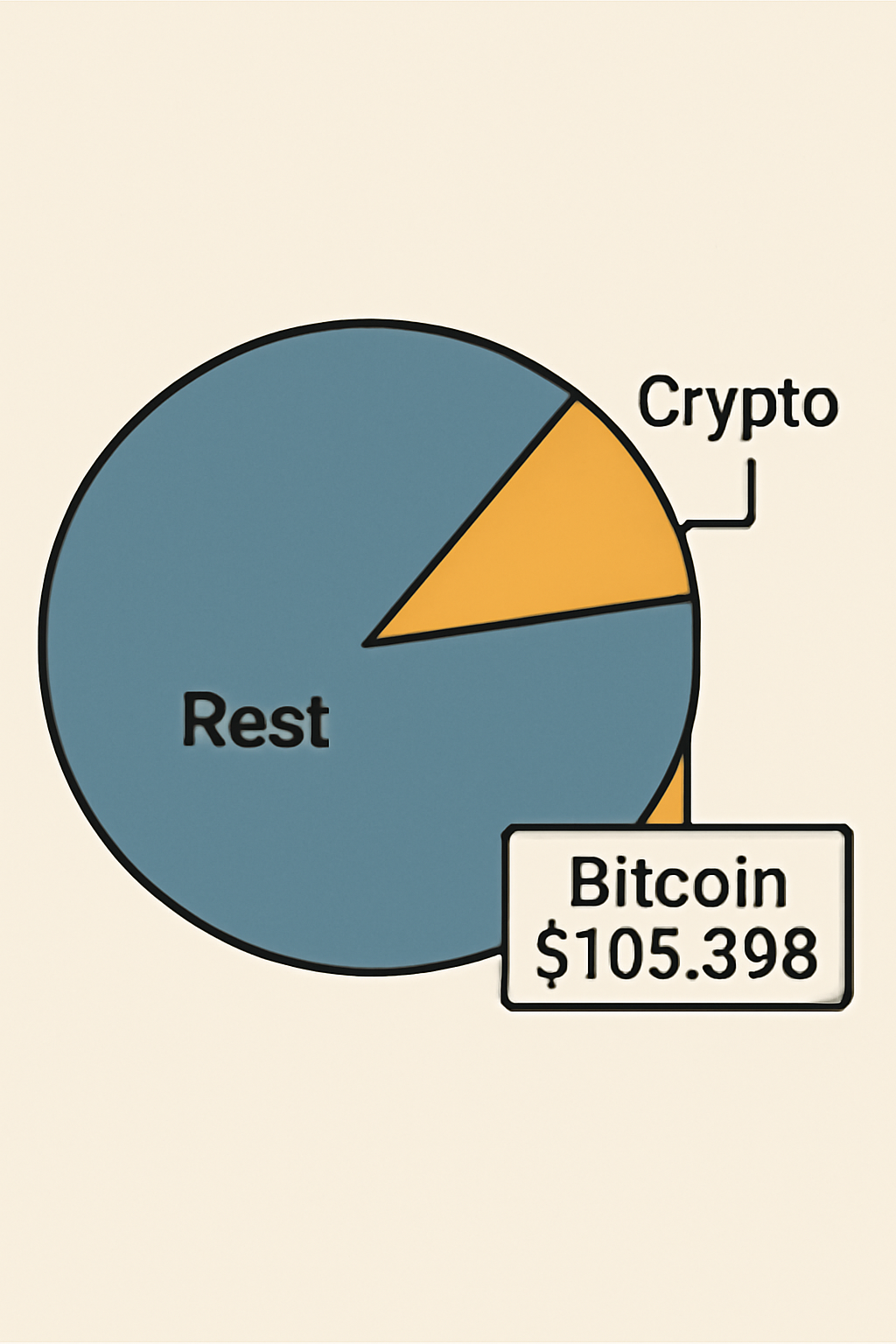

In 2025, the landscape for cryptocurrency in 401k plans has shifted dramatically. With Bitcoin trading at $106,388.00, regulatory changes have opened the doors for everyday investors to integrate digital assets into their retirement portfolios. If you’re looking to add crypto to your 401k, you’re not alone - and you’re right on time as innovation meets opportunity in retirement planning.

The New Era: Crypto Access in Your 401(k)

Following an executive order signed by President Donald Trump in August 2025, both the Department of Labor (DOL) and Securities and Exchange Commission (SEC) have issued guidance that allows employers and plan sponsors to include private assets like cryptocurrencies in 401(k) plans. This move is a milestone for retirement diversification and aligns with the growing demand for alternative investments among forward-thinking savers.

This regulatory green light means more plans are rolling out crypto options. However, navigating these new choices requires clarity on process, risk management, and compliance. Let’s dig into what this means for you as an investor.

Step-by-Step: How to Add Crypto to Your 401(k) in 2024-2025

How to Add Cryptocurrency to Your 401(k): A Visual Step-by-Step Guide (2024-2025)

The process of integrating digital assets in your retirement plan is now more streamlined than ever. Here’s what you need to know:

- Verify Plan Eligibility: Start by contacting your HR department or plan administrator. Not every employer-sponsored plan offers crypto yet - check if yours does.

- Review Investment Options: Some plans enable direct purchases of coins like Bitcoin or Ethereum; others offer exposure via cryptocurrency funds or ETFs.

- Understand Fees: Digital asset trades can incur higher fees than traditional investments. Look out for trading costs and custodial charges specific to crypto holdings.

- Assess Your Risk Tolerance: Crypto remains volatile - with Bitcoin recently swinging between $101,543.00 and $106,552.00. Limit allocation (often capped at 5% of your portfolio) unless you have a high risk appetite.

- Diversify Smartly: Even with newfound access, most experts recommend keeping your crypto exposure modest within your overall retirement strategy.

If your plan doesn’t support digital assets yet, alternatives like self-directed IRAs or taxable brokerage accounts may be worth exploring. For more on these routes, see our guides on Bitcoin integration steps.

Navigating Risks and Regulatory Updates

The Department of Labor continues to urge fiduciaries to exercise “extreme care” before adding crypto options. This isn’t just bureaucratic caution - it reflects real concerns about volatility, security breaches, and evolving tax treatment around digital assets. As adoption grows post-executive order, expect further guidance from regulators throughout late 2025 and beyond.

AARP, the Government Accountability Office (GAO), and leading financial advisors agree: limit exposure until you fully understand both the upside potential and downside risks of integrating digital assets in retirement plans.

The Case for Crypto Retirement Diversification

The core argument for including cryptocurrency in your 401(k) is diversification. Digital assets don’t always move in sync with stocks or bonds - potentially reducing portfolio risk over time when used judiciously. With Bitcoin holding strong above $100,000 this year ($106,388.00 as of November 2025), there’s no denying its growing influence as an alternative store of value within long-term investment strategies.

Still, it’s essential to remember that crypto retirement diversification is not a magic bullet. The same volatility that makes assets like Bitcoin attractive for growth also means sharp corrections can and do happen. You’ll want to keep a close eye on your portfolio allocation and rebalance periodically, especially if crypto outperforms or underperforms your other holdings.

Security and Custody: Protecting Your Digital Assets

One of the most critical aspects of adding cryptocurrency to your 401(k) is security. Unlike stocks or mutual funds, digital assets require specialized custody solutions. Most plan providers now partner with regulated custodians who use cold storage, multi-signature wallets, and robust insurance policies. Before allocating funds, ask your plan administrator about their security protocols and how they manage private keys.

You should also enable two-factor authentication (2FA) on any platform where you access your retirement account. Even the best custodians aren’t immune to breaches, so personal vigilance is always part of the equation.

Tax Efficiency and Withdrawal Rules

Adding crypto to your 401(k) preserves the core tax advantages of retirement accounts: contributions are pre-tax (traditional) or post-tax (Roth), and gains grow tax-deferred until withdrawal. However, distributions in retirement will be taxed according to regular 401(k) rules, regardless of whether you hold Bitcoin or an S and amp;P 500 index fund.

If you’re considering rolling over to a self-directed IRA for broader crypto access, be sure to review IRS guidelines carefully, mistakes here can trigger penalties or unexpected taxes.

What’s Next? Evolving Access and Best Practices

The landscape for integrating digital assets in retirement plans is moving fast. More employers are expected to offer crypto options as demand grows and regulatory clarity improves. If you’re eager to stay ahead:

- Monitor Regulatory Updates: Regulatory guidance will continue evolving through late 2025 and into 2026. Stay informed by checking trusted news sources or subscribing to updates from your plan provider.

- Review Plan Changes Annually: As more asset types become available, including private equity and real estate, review your plan’s investment menu during open enrollment each year.

- Consult with Experts: A financial advisor familiar with both crypto markets and retirement planning can help tailor strategies for your specific goals and risk tolerance.

Final Thoughts: Is Crypto Right for Your Retirement?

If you’re ready to add crypto exposure, whether through direct purchase or a managed fund, remember that patience pays off in retirement investing. Allocate modestly at first (most plans cap crypto at around 5%), monitor performance closely, and adjust as needed based on both market moves and regulatory shifts.

The door is now open for mainstream adoption of cryptocurrency in 401(k)s, and while the path isn’t risk-free, it offers a new dimension for building long-term wealth. For more detailed walkthroughs on specific cryptocurrencies like Bitcoin in your retirement account, check out our practical guide here.

No comments yet. Be the first to share your thoughts!