As inflation continues to chip away at traditional retirement savings in 2026, savvy investors are eyeing 401k to bitcoin ira rollover strategies to unlock inflation-beating returns. With Bitcoin holding steady at $67,576 amid market fluctuations, a Bitcoin IRA positions your nest egg in an asset that has historically outpaced fiat currencies and even gold during economic uncertainty. This move isn’t just speculative; it’s a calculated shift toward bitcoin retirement accounts 2026 that leverage crypto’s scarcity and growing institutional adoption.

Why Bitcoin IRAs Trump Inflation in Your Retirement Portfolio

Traditional 401ks locked into bonds and stocks struggle against persistent inflation, often delivering real returns below 2% after fees and erosion. Bitcoin, however, acts as digital gold with a fixed supply of 21 million coins, making it a prime candidate for an inflation proof 401k crypto strategy. At its current price of $67,576, BTC has demonstrated resilience, bouncing from a 24-hour low of $66,702 to resist broader market dips. Providers like Bitcoin IRA and Swan Bitcoin emphasize that self-directed IRAs allow tax-deferred growth on crypto holdings, potentially compounding your rollover into substantial wealth by retirement.

Consider the mechanics: a direct rollover keeps your funds tax-free, avoiding the 20% withholding on indirect transfers. This preserves every dollar for Bitcoin allocation. Yet, volatility demands discipline; Bitcoin’s 24-hour range from $66,702 to $69,111 underscores the need for a long-term horizon. Forward-thinking advisors recommend allocating no more than 5-10% initially to mitigate swings while capturing upside.

Bitcoin (BTC) Price Prediction 2027-2032

Bullish, Average, and Bearish Scenarios for Inflation-Beating Returns in Bitcoin IRA Investments (Baseline: $67,576 in 2026)

| Year | Minimum Price (Bearish) | Average Price | Maximum Price (Bullish) |

|---|---|---|---|

| 2027 | $80,000 | $150,000 | $250,000 |

| 2028 | $120,000 | $350,000 | $600,000 |

| 2029 | $200,000 | $500,000 | $900,000 |

| 2030 | $300,000 | $700,000 | $1,200,000 |

| 2031 | $450,000 | $950,000 | $1,500,000 |

| 2032 | $600,000 | $1,200,000 | $2,000,000 |

Price Prediction Summary

Bitcoin is forecasted to deliver strong growth from 2027 to 2032, with average prices climbing from $150K to $1.2M, fueled by halving cycles and adoption. Wide ranges account for volatility, offering high potential ROI for Bitcoin IRA holders but with bearish risks from regulation and macro downturns.

Key Factors Affecting Bitcoin Price

- 2028 Bitcoin halving sparking bull cycle

- Rising institutional adoption via ETFs and corporate treasuries

- Regulatory clarity and global acceptance

- Technological upgrades enhancing scalability and use cases

- Macroeconomic pressures like inflation favoring BTC as store of value

- Potential risks from competition, hacks, or strict regulations

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis.

Actual prices may vary significantly due to market volatility, regulatory changes, and other factors.

Always do your own research before making investment decisions.

Assessing Eligibility for a Self-Directed 401k Bitcoin Rollover

Before diving into the process, confirm you’re eligible for a 401k to bitcoin ira rollover. Most plans allow rollovers after leaving your employer, whether through job change, retirement, or reaching age 59½. Contact your 401k administrator to verify no restrictions apply, especially if still employed. IRS rules permit one rollover per 12-month period per account, starting from the date you receive funds, so opt for direct transfers to custodians like Equity Trust or IRA Financial.

Gather essentials: your latest 401k statement, Social Security number, and beneficiary details. Review custodian fees; top Bitcoin IRA platforms charge 1-2% annually plus transaction costs, far lower than hidden 401k expense ratios averaging 1.5%. Fidelity notes crypto IRAs are now mainstream, but choose FDIC-insured partners for fiat holdings and cold storage for BTC security. This preparation phase typically takes 1-2 weeks and sets the stage for seamless execution.

Bitcoin’s path to $100,000 isn’t guaranteed, but its inflation hedge properties make it indispensable for 2026 retirement planning.

Step-by-Step: Opening Your Bitcoin IRA and Initiating the Rollover

Start by selecting a reputable custodian specializing in crypto 401k alternatives. Platforms like Swan Bitcoin or Bitcoin IRA streamline onboarding with digital applications. Complete the self-directed IRA setup, designating Bitcoin as the primary asset. Expect approval within days, as they handle IRS compliance for alternative investments.

- Open the account: Provide ID verification and link your bank for any cash needs.

- Request direct rollover: Your new IRA custodian issues instructions to your 401k provider, ensuring funds move IRA-to-IRA without touching your hands.

- Confirm receipt: Funds arrive as cash in 5-10 business days; immediately allocate to Bitcoin at market price, currently $67,576.

Swan Bitcoin outlines this precisely: post-rollover, purchase BTC in the vault for secure, insured storage. Avoid indirect rollovers to dodge taxes and penalties. Capitalize highlights that employer plans often resist crypto, making the IRA switch essential for control.

With funds secured, monitor your position as Bitcoin navigates 2026’s regulatory landscape. Upcoming halvings and ETF inflows could propel prices higher, amplifying your returns. This foundational half positions you ahead of the curve.

Once your rollover completes, the real work begins: strategically deploying those funds into Bitcoin at its current $67,576 price point. Resist the urge to time the market; dollar-cost averaging smooths out volatility seen in the recent 24-hour swing from $66,702 to $69,111. Custodians like IRA Financial enable seamless BTC purchases within the IRA, locking in tax advantages while your holdings compound.

Mastering Risk Management in Your Self-Directed 401k Bitcoin Setup

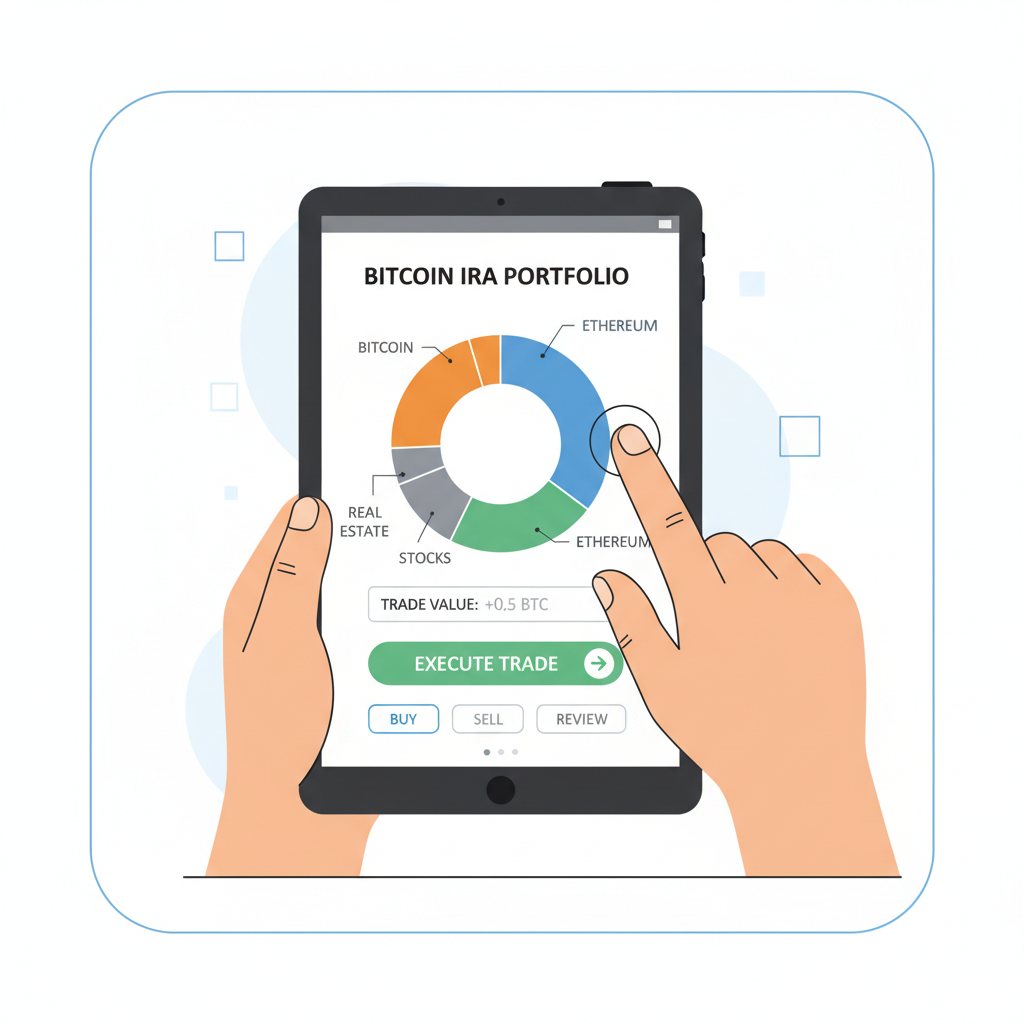

Bitcoin’s volatility is no secret, but dismissing it outright ignores its track record as an inflation proof 401k crypto powerhouse. At $67,576, BTC sits resilient against fiat debasement, yet sharp drawdowns demand safeguards. Limit exposure to 5-10% of your total retirement portfolio initially, diversifying with stablecoins or Ethereum if your custodian allows. Equity Trust stresses cold storage and multi-signature wallets to fortify against hacks, while Accuplan FAQs highlight insurance up to $250 million on many platforms.

Implement stop-loss orders where possible, though IRA restrictions vary. Regularly review allocations quarterly, rebalancing to capture gains without emotional selling. Bitcoin Magazine’s guide underscores that halvings, next in 2028, historically ignite bull runs; position now to ride that wave tax-deferred. This disciplined approach turns crypto 401k alternatives into reliable wealth engines, not gambles.

Rebalance Your Bitcoin IRA Portfolio for 2026: Risk Checks, DCA & Quarterly Reviews

Tax Nuances and Compliance for Bitcoin Retirement Accounts 2026

Direct rollovers sidestep the 10% early withdrawal penalty and 20% mandatory withholding that plague indirect moves. IRS guidelines, as outlined by Bitcoin IRA, treat crypto like any IRA asset: gains grow tax-deferred in traditional setups or tax-free in Roth conversions. Watch for UBIT if using leveraged trades, though spot BTC holds rarely trigger it. Fidelity Investments warns of state tax variances, so document every transaction meticulously.

For 2026, proposed regulations may clarify crypto IRA reporting, potentially easing audits. Convert portions to Roth IRAs over time if in lower brackets, paying taxes upfront for perpetual tax-free growth. Bitcoin financial services notes custodians handle Form 1099-R issuance, simplifying your filings. Proactive tax planning preserves more of your $67,576 BTC exposure for compounding.

Providers like Swan Bitcoin offer tools for seamless conversions, ensuring compliance amid evolving rules. Pair this with beneficiary updates to shield assets from probate, securing legacy wealth.

Scaling Up: Advanced Strategies for Inflation-Beating Growth

Beyond basics, explore stacking sats via recurring buys post-rollover. As Bitcoin hovers at $67,576, institutional inflows from ETFs bolster its floor, outpacing traditional assets mired in low yields. Self-directed 401k bitcoin enthusiasts layer in momentum trades during uptrends, using technical patterns like swing lows near $66,702 for entries.

Monitor macro cues: Fed rate cuts and geopolitical tensions amplify BTC’s safe-haven appeal. IRA Financial enables Ethereum diversification, hedging BTC-specific risks while chasing DeFi yields tax-sheltered. Aim for 7-10% annual real returns net of fees, dwarfing bond ladders. This isn’t passive indexing; it’s active stewardship for bitcoin retirement accounts 2026.

Track performance against benchmarks quarterly, adjusting as halvings approach. Platforms provide dashboards for real-time oversight, empowering data-driven tweaks.

Discipline beats speculation every time in crypto IRAs – hold through dips, reap the cycles.

Your 401k to Bitcoin IRA rollover transforms stagnant savings into a dynamic shield against inflation. With BTC at $67,576 proving its mettle, execute methodically, manage risks sharply, and watch compounding work its magic through 2026 and beyond. Forward-thinking investors who act now position for outsized retirement security in an uncertain world.