As a self-employed professional eyeing Bitcoin's potential in your retirement strategy, you're in a prime position with a Solo 401k. With Bitcoin trading at $86,314 today, self directed 401k crypto investments offer a compelling way to harness this asset's growth while optimizing taxes. Solo 401k bitcoin setups let you, as both employer and employee, maximize contributions and enjoy tax advantages tailored for independent contractors.

I've advised countless freelancers and consultants on bitcoin solo 401k 2025 strategies, and the appeal lies in the flexibility. Unlike traditional 401ks, a Solo 401k empowers you to direct funds toward alternative assets like cryptocurrency, provided you follow IRS guidelines. This structure is ideal for those with net earnings from self-employment, allowing higher limits than IRAs.

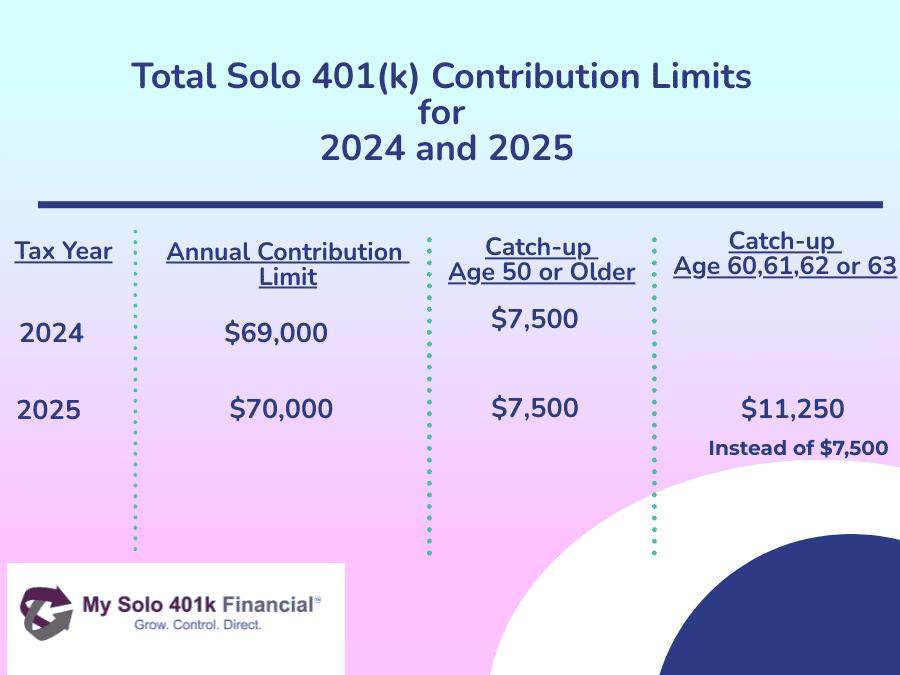

Unlocking 2025 Contribution Limits for Maximum Bitcoin Exposure

For 2025, the IRS sets the employee elective deferral at $23,500 if under 50. Catch-up contributions add firepower: $7,500 for ages 50-59 and 64 and, but a standout $11,250 super catch-up for those 60-63. As your own employer, layer on profit-sharing up to 25% of compensation, capping total contributions at $70,000 excluding catch-ups. Compensation for these calculations maxes at $350,000, so high earners can push limits further.

Picture a consultant earning $150,000 net: defer $23,500 as employee, contribute about $30,000 as employer (20% effectively after adjustments), totaling around $53,500 parked toward Bitcoin. This dwarfs IRA caps at $7,500. For bitcoin retirement tax benefits, these pre-tax dollars grow sheltered, amplifying compound returns at Bitcoin's current $86,314 price point.

Navigating Tax Treatment in Your Solo 401k Cryptocurrency Rules

Solo 401k cryptocurrency rules hinge on Traditional versus Roth options. Traditional contributions slash your current taxable income, with Bitcoin gains tax-deferred until withdrawal, taxed as ordinary income then. Roth flips it: pay taxes now for tax-free qualified distributions later, perfect if you anticipate higher brackets or Bitcoin's ascent from $86,314.

Read more on tax implications of holding crypto in your 401k. In-plan Roth conversions offer flexibility, converting traditional balances to Roth within the plan, though you'll owe taxes on the converted amount. Distributions before 59½ trigger penalties, so time horizons matter. The DOL's neutral stance on crypto in 401ks greenlights fiduciaries like you to include it prudently.

"Bitcoin's volatility demands disciplined allocation, but in a Solo 401k, tax deferral turns that risk into a retirement accelerator. "

Prohibited transactions are a pitfall; no personal custody of Bitcoin allowed. Stick to compliant vehicles to avoid disqualification.

Strategic Ways to Invest in Bitcoin Through Your Self Directed 401k

Direct Bitcoin holding? Not in a Solo 401k. Instead, channel funds via Bitcoin ETFs or trusts that mirror performance without custody issues. These wrappers comply with IRS and DOL regs, letting your contributions ride Bitcoin's momentum from $86,314.

Check out guidance on how to use a self-directed Solo 401k for crypto investments. Self-directed custodians handle Bitcoin exposure seamlessly, often with low fees. Allocate 5-15% initially, scaling as conviction builds, always prioritizing diversification.

Bitcoin (BTC) Price Prediction 2026-2031 for Solo 401(k) Strategies

Forecasts for self-employed investors planning tax-advantaged retirement portfolios amid market cycles and adoption trends

| Year | Minimum Price (USD) | Average Price (USD) | Maximum Price (USD) |

|---|---|---|---|

| 2026 | $70,000 | $110,000 | $160,000 |

| 2027 | $85,000 | $130,000 | $190,000 |

| 2028 | $100,000 | $160,000 | $240,000 |

| 2029 | $130,000 | $200,000 | $310,000 |

| 2030 | $170,000 | $260,000 | $410,000 |

| 2031 | $220,000 | $340,000 | $530,000 |

Price Prediction Summary

From a 2025 baseline of ~$86,000, Bitcoin is projected to grow steadily through 2031, with average prices rising 3x+ by decade's end. Bullish max scenarios reflect ETF inflows and adoption; min ranges account for corrections. Ideal for long-term Solo 401(k) holding with tax-deferred growth potential yielding 200-500% ROI.

Key Factors Affecting Bitcoin Price

- Institutional adoption via Bitcoin ETFs and retirement plans

- Post-2024 halving supply constraints and 2028 halving anticipation

- Regulatory neutrality from DOL/IRS enabling crypto in 401(k)s

- Macroeconomic shifts like lower rates boosting risk assets

- Technological scalability (e.g., Lightning Network) and global use cases

- Competition from altcoins but BTC dominance persisting

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis. Actual prices may vary significantly due to market volatility, regulatory changes, and other factors. Always do your own research before making investment decisions.

Reporting kicks in with Form 5500-EZ if assets top $250,000, plus 1099-R for Roth moves. Partner with a specialist to sidestep errors; I've seen overlooked filings cost dearly.

Staying compliant keeps your Solo 401k humming smoothly, preserving those bitcoin retirement tax benefits you've worked hard to secure. Beyond forms, annual valuations and nondiscrimination testing aren't required for one-participant plans, simplifying administration compared to group 401ks. This lean setup lets self-employed folks like you focus on Bitcoin's upside from its current $86,314 perch.

These limits pack a punch for high earners. Say you're a 62-year-old freelancer netting $200,000: snag the $23,500 deferral, $11,250 super catch-up, and $40,000 employer contribution (20% after self-employment tax tweaks), hitting $74,750 total. That's serious firepower for self directed 401k crypto plays, far outpacing SEP IRAs or simple plans.

I've guided clients through these calculations, and the math often surprises them. Profit-sharing percentages adjust for self-employment taxes; use 20% of net business income as a rule of thumb for simplicity. Tools from custodians like Fidelity or specialized providers crunch exact figures, ensuring you max out without IRS flags.

Risk Management in Volatile Bitcoin Markets

Bitcoin at $86,314 tempts aggressive bets, but solo 401k cryptocurrency rules demand prudence. Volatility swings demand dollar-cost averaging: funnel monthly contributions into ETFs regardless of price dips. Diversify beyond pure BTC; pair with Ethereum funds or broad crypto indexes to temper risk.

In my experience, over-allocating past 10-20% invites sleepless nights, even with tax shelters. Rebalance annually, selling high performers to buy laggards within the plan. Regulatory shifts, like potential DOL guidance tightening crypto access, loom; stay informed via trusted advisors.

"Discipline beats FOMO every time in retirement planning. Bitcoin's long-term trajectory shines brighter with steady, tax-advantaged accumulation. "

Custodial choice matters. Seek self-directed providers versed in crypto, offering robust security like multi-sig wallets for underlying trusts. Fees erode returns, so compare expense ratios; some ETFs hover under 0.25% annually.

Overcoming Common Hurdles for Self-Employed Investors

Prohibited transactions top the pitfalls list: lending plan assets or guaranteeing investments voids tax status. I've witnessed near-misses where clients eyed personal wallets; always route through qualified intermediaries. Plan loans up to $50,000 offer liquidity without taxes, but default risks disqualification.

Rollovers from prior IRAs or 401ks supercharge your Bitcoin base. Direct transfers preserve tax treatment; indirect ones risk withholding. For Roth purists, ladder conversions over years to manage tax hits.

Setting up demands paperwork: adopt a plan document, secure an EIN if needed, and designate trustees. Costs run $500-$2,000 initially, with ongoing $100-$300 yearly. Worth it for the contribution muscle and bitcoin solo 401k 2025 flexibility.

As Bitcoin holds steady at $86,314, self-employed pros hold the keys to blending crypto's growth with retirement security. Pair strategic contributions, compliant investments, and vigilant oversight for a portfolio that endures. Reach out to a certified advisor attuned to these nuances; the right moves today compound into lasting wealth tomorrow.

No comments yet. Be the first to share your thoughts!