The 2026 DOL safe harbor for crypto

On March 30, 2026, the Department of Labor (DOL) issued a proposed rule that fundamentally alters the regulatory landscape for retirement plan fiduciaries considering cryptocurrency. The proposal creates a "safe harbor" provision, effectively moving crypto and other alternative assets from a presumed prohibited transaction to a permissible investment option, provided specific due diligence and monitoring steps are followed. This shift follows an executive order signed last summer that cleared the path for private equity and crypto to enter 401(k) portfolios.

The core mechanism of the rule is risk mitigation through process. Fiduciaries must now treat crypto assets with the same rigor as traditional stocks or bonds, conducting thorough investigations into the asset's viability and the service provider's integrity. The DOL emphasizes that while the asset class is no longer banned, the burden of proof for its suitability rests entirely on the plan sponsor.

This regulatory pivot reflects a broader industry push for diversification, with proponents arguing that alternative assets can enhance returns. Yet, the DOL's cautionary tone underscores the volatility inherent in crypto markets. As Bitcoin and other digital assets continue to experience significant price swings, fiduciaries must weigh the potential for growth against the stark reality of capital preservation in retirement accounts.

For detailed guidance on the proposed rule's text and comment periods, refer to the DOL's official announcement.

The proposal also addresses fee transparency, a longstanding concern in the 401(k) space. Plan sponsors must ensure that any crypto-related fees are reasonable and clearly disclosed to participants. This requirement aims to prevent the erosion of retirement savings through hidden costs associated with managing high-risk, high-volatility assets.

While the rule is still in the proposal stage, its implications are immediate. Plan providers are already updating their platforms to accommodate these new investment options, and fiduciaries are beginning to assess their current portfolios for compliance. The coming months will likely see a surge in discussions about how to integrate these assets responsibly into retirement planning strategies.

Fiduciary duties and investment risks

The Department of Labor’s recent proposals have shifted the regulatory landscape, allowing plan sponsors to include cryptocurrency and other alternative assets in 401(k) plans. However, this expansion does not absolve fiduciaries of their strict legal obligations. Under ERISA, sponsors must still prove that every investment option is prudent, diversified, and low-cost. For volatile digital assets, meeting these criteria is exceptionally difficult.

The stakes are immense. U.S. 401(k) plans hold over $7 trillion in assets, meaning even a small allocation to crypto can significantly impact market liquidity and individual retirement outcomes. Reuters and CoinDesk report that while the executive order clears the path for these investments, the burden of proof remains on plan sponsors to justify their inclusion.

The Prudence Challenge

Cryptocurrency’s historical volatility clashes with the fiduciary standard of prudence. Sponsors must demonstrate that crypto does not unduly expose participants to unnecessary risk. This requires rigorous due diligence, often involving third-party experts, to evaluate the asset’s role in a diversified portfolio. Without clear long-term data, proving prudence is a legal minefield.

Cost and Diversification

Beyond volatility, fiduciaries must address fees and diversification. Crypto funds often carry higher expense ratios than traditional index funds, potentially violating the low-cost requirement. Additionally, adding a highly correlated, high-risk asset to a retirement portfolio can undermine diversification goals. Sponsors must carefully model these impacts to avoid breaches of fiduciary duty.

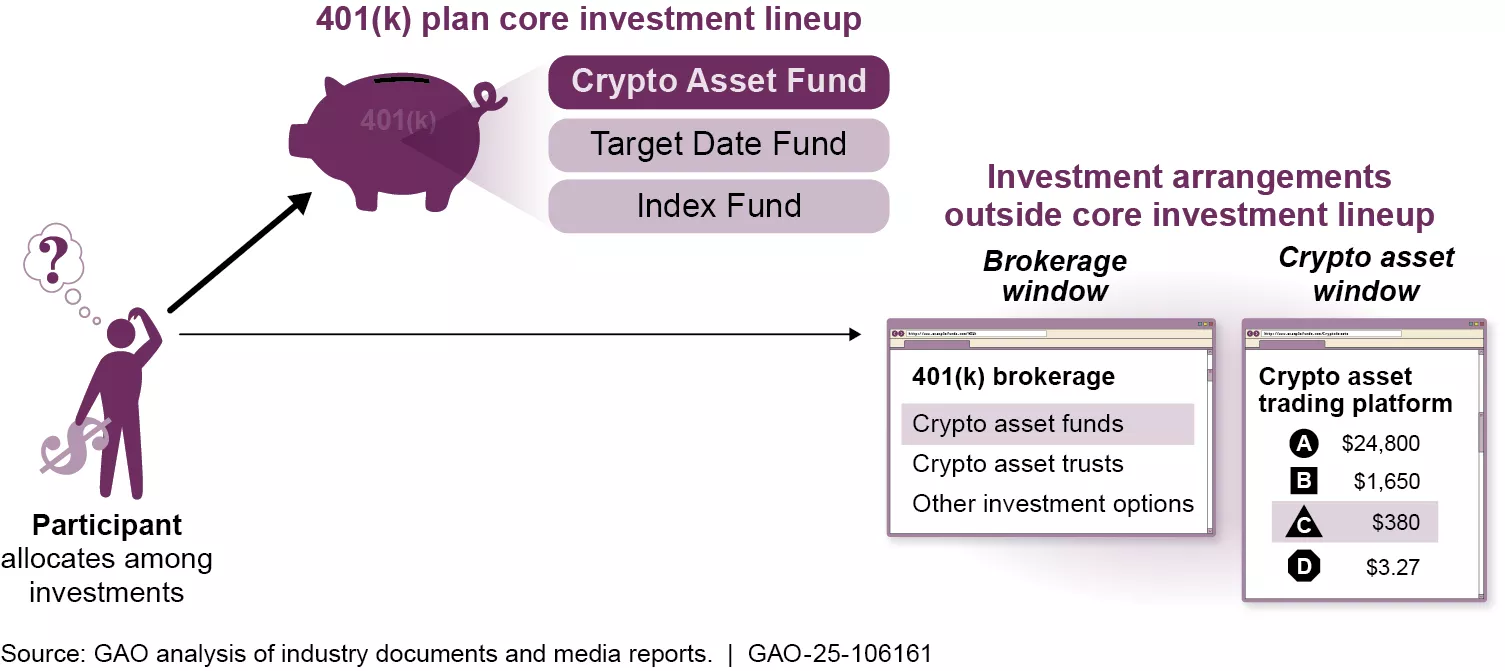

Provider models and crypto access paths

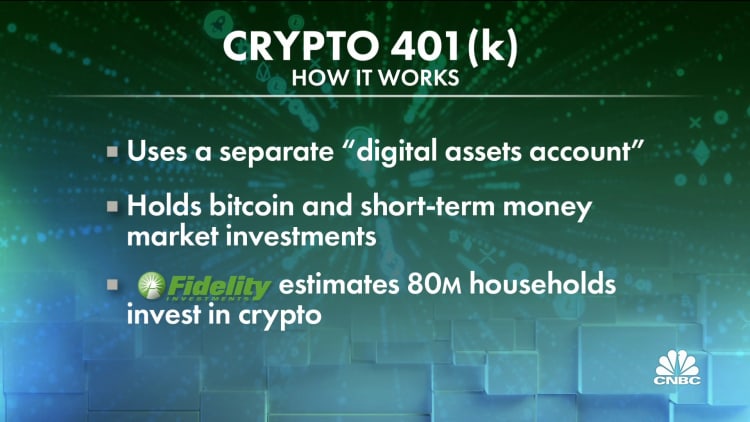

The Department of Labor’s proposal to allow cryptocurrencies in 401(k) plans has triggered a bifurcation in provider strategy. Legacy custodians and specialized platforms are structuring these options differently, primarily distinguishing between direct crypto holdings and crypto-focused funds. Understanding this structural difference is critical for fiduciaries assessing compliance and risk.

Legacy providers like Fidelity are largely restricting crypto exposure to crypto-focused exchange-traded funds (ETFs). This approach aligns with traditional fiduciary standards by offering regulated, custodied assets that fit within existing plan governance frameworks. In contrast, specialized platforms such as ForUsAll are enabling direct cryptocurrency holdings. This model allows participants to buy and hold assets like Bitcoin and Ethereum directly within their 401(k) accounts, offering broader asset access but requiring distinct compliance and custody mechanisms.

The fee structures also diverge significantly between these models. Specialized platforms often advertise low trading fees, such as 0.15%, with no minimums or setup fees, aiming to attract participants seeking direct exposure. Legacy providers typically charge higher expense ratios associated with managing ETF options, though they may bundle these costs into broader administrative fees. The choice between these models impacts both the participant’s cost basis and the plan sponsor’s fiduciary liability.

| Provider Type | Asset Access | Fee Structure | Custody Model |

|---|---|---|---|

| Legacy (e.g., Fidelity) | Crypto ETFs only | Standard ETF expense ratios | Traditional securities custody |

| Specialized (e.g., ForUsAll) | Direct Bitcoin, Ethereum | Low trading fees (e.g., 0.15%) | Digital asset custodians |

Fiduciaries must evaluate which model best serves their participants’ needs while adhering to the Department of Labor’s guidelines. The shift toward direct holdings represents a significant change in retirement plan architecture, demanding robust oversight and clear participant education. As the regulatory landscape evolves, providers will likely refine their offerings to balance innovation with compliance.

2026 Contribution Limits and Market Volatility

The regulatory landscape for retirement plans shifted significantly in early 2026 as the IRS announced updated contribution limits. The standard elective deferral limit for 401(k) plans rose to $24,500, an increase of $1,000 from the 2025 threshold of $23,500. For participants aged 50 and older, the catch-up contribution limit increased by $500 to $7,500. These adjustments, driven by inflation indexing, expand the capital available for deployment into alternative assets, including cryptocurrency funds, but they also amplify the potential downside for fiduciaries managing plan risk.

This influx of capital intersects with a period of heightened Bitcoin volatility. In the first months of 2026, Bitcoin experienced a sharp correction, falling nearly 20% year-to-date and retreating from its October all-time high near $126,000. This price action underscores the speculative nature of crypto assets within a retirement context. While the executive order permitting alternative assets in 401(k) plans opened the door for actively managed crypto funds, the recent market turbulence highlights the fiduciary challenge of balancing growth potential against the preservation of retirement savings.

The combination of higher contribution limits and volatile asset prices creates a complex environment for plan sponsors. The Department of Labor’s ongoing proposals regarding fiduciary duties for alternative investments require careful navigation. As more capital flows into these plans, the need for robust risk management frameworks becomes critical. The recent price swings serve as a reminder that while regulatory barriers are lowering, the inherent risks of crypto assets remain substantial for long-term retirement portfolios.

Steps to evaluate a crypto 401k plan

The Department of Labor’s March 2026 proposal establishes a safe harbor for fiduciaries adding crypto and alternative assets to 401(k) plans, signaling a regulatory shift toward permitting these high-risk holdings [[src-serp-3]]. However, this permission does not eliminate the inherent volatility or the fiduciary duty to protect retirement assets. Evaluating a crypto 401k plan requires a rigorous audit of fees, liquidity, and personal risk tolerance before any capital is allocated.

Crypto 401k plans often carry higher administrative and trading fees than traditional stock or bond options. Some providers advertise low trading fees (e.g., 0.15%), but you must verify if setup fees, custody fees, or annual platform charges apply [[src-serp-4]]. High fees erode long-term returns, especially in a volatile asset class. Ensure the total cost of ownership is transparent and competitive.

Unlike public equities, some crypto or alternative asset options may have restricted redemption windows. Check if the plan allows daily trading or if withdrawals are subject to lock-up periods. Illiquidity can trap capital during market downturns, making it impossible to exit positions when needed. Confirm that the plan’s liquidity terms align with your retirement timeline.

Fiduciaries must ensure that adding crypto meets the "prudent investor" standard under ERISA. Review the plan’s prospectus for clear risk disclosures regarding price volatility, regulatory uncertainty, and cybersecurity threats. If the plan lacks robust educational materials or risk warnings, it may indicate a higher exposure to speculative behavior. Ensure the provider offers transparent reporting and compliance support.

Crypto assets can experience extreme price swings, as seen with Bitcoin’s 20% year-to-date decline in early 2026 [[src-serp-5]]. Determine if your retirement portfolio can withstand significant drawdowns without jeopardizing your financial security. Crypto should generally represent a small, speculative portion of a diversified portfolio, not a core holding. Consult a financial advisor to model how crypto allocation impacts your long-term retirement projections.

No comments yet. Be the first to share your thoughts!