The 2026 DOL safe harbor explained

The Department of Labor’s March 2026 proposal fundamentally alters the regulatory landscape for retirement plans by introducing a proposed safe harbor for fiduciaries who add cryptocurrency and other alternative assets to 401(k) plans. This is not a mandate requiring plan sponsors to offer crypto, nor is it a blanket approval of these volatile assets. Instead, it establishes a legal shield for fiduciaries who can demonstrate that offering crypto serves the interests of plan participants and beneficiaries, provided they adhere to strict due diligence and risk management protocols.

Historically, the DOL maintained a prohibition-like stance, viewing cryptocurrency as inherently speculative and unsuitable for retirement savings. The proposed rule marks a significant shift from this precautionary approach to a more permissive framework, contingent on rigorous fiduciary oversight. Plan sponsors must now navigate a complex web of requirements, including assessing the liquidity of crypto holdings, evaluating the operational capacity of third-party administrators, and ensuring that crypto offerings do not compromise the overall diversification and stability of the retirement portfolio.

The Department of Labor's March 2026 proposal creates a legal shield for plan sponsors who add crypto, provided they follow strict due diligence steps.

For fiduciaries, the immediate implication is a heightened burden of proof. Offering crypto is no longer automatically a breach of fiduciary duty, but failing to document a comprehensive risk assessment can lead to severe penalties. This regulatory evolution requires plan sponsors to engage with specialized custodians and legal counsel to ensure compliance with the new standards. The goal of the DOL is to allow retirement plans to keep pace with evolving financial markets while protecting participants from undue risk.

The proposed rule also addresses the operational challenges of holding digital assets. Fiduciaries must ensure that the recordkeeping systems are robust enough to track crypto transactions accurately and that the fees associated with crypto offerings are reasonable and transparent. This includes evaluating the security measures of crypto custodians and understanding the potential for market volatility to impact retirement savings. The DOL’s stance reflects a recognition that excluding crypto entirely may no longer be in the best interest of participants who seek exposure to emerging asset classes.

While the proposal is still in the comment period, its direction signals a clear intent to modernize retirement plan regulations. Plan sponsors are advised to monitor the final rule closely and prepare their investment policy statements to accommodate potential crypto offerings. The safe harbor provides a pathway for innovation, but it demands a disciplined, evidence-based approach to fiduciary decision-making. Those who fail to adapt may find themselves exposed to regulatory scrutiny and participant dissatisfaction in the years to come.

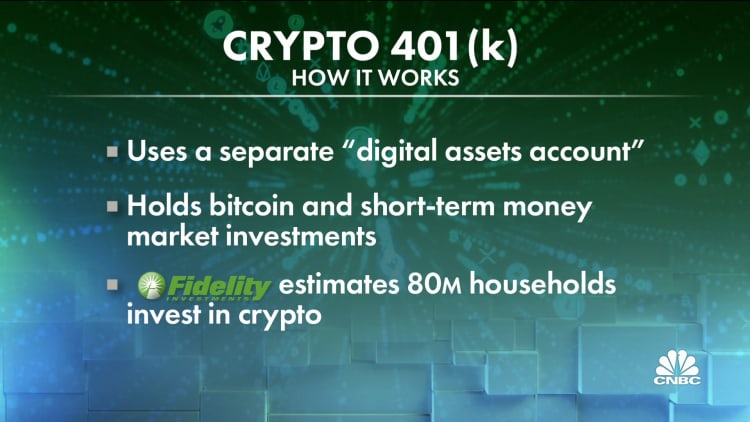

Three paths for crypto in your plan

The 2026 Department of Labor rule change does not mandate cryptocurrency in retirement plans, nor does it automatically include Bitcoin in your 401(k). Instead, it removes the regulatory fear that previously discouraged plan sponsors from offering digital assets. This shift opens three distinct mechanisms for accessing crypto, each carrying different fiduciary responsibilities and risk profiles.

Self-directed brokerage windows

A self-directed brokerage window allows participants to divert a portion of their existing contributions into a wider range of investments, including individual stocks, mutual funds, and potentially cryptocurrencies. Under this structure, the employer does not add a new crypto fund; rather, they permit employees to use their current balance to purchase crypto through a connected brokerage platform.

This path places the highest burden of due diligence on the employee. While the employer is not directly selecting the crypto asset, they must ensure the brokerage vendor is reputable and that the window is properly documented. This method offers maximum flexibility but requires participants to actively manage their own crypto exposure within the tax-advantaged account.

Dedicated alternative asset menus

Some plan providers are developing dedicated menus for alternative assets, including regulated crypto funds or exchange-traded products. These menus are curated by the plan sponsor and the third-party administrator, who perform the initial due diligence on custody and compliance. Participants can then select these specific options from the plan’s investment lineup, similar to how they choose between large-cap and small-cap funds.

This approach centralizes the fiduciary risk with the plan sponsor. By selecting a pre-vetted crypto option, the employer signals that they have reviewed the custody solution and regulatory standing of the asset. For employees, this simplifies the process, as they do not need to navigate external brokerage accounts to hold crypto within their 401(k).

Direct rollovers

Direct rollovers allow individuals moving between jobs or converting a traditional 401(k) into a Roth IRA to include crypto assets if the receiving plan permits it. While most employer-sponsored 401(k) plans do not currently accept direct rollovers of cryptocurrency, self-directed IRAs often do. This path is less about new plan features and more about the flexibility of retirement accounts.

If a plan sponsor chooses to offer a crypto option, it must be compatible with rollover mechanics. This means the plan’s recordkeeper must be able to track the cost basis and value of the crypto holdings accurately. For now, this path is most viable for those willing to move their funds into a self-directed IRA that explicitly allows digital assets, rather than staying within a traditional employer plan.

Comparison of access methods

The table below outlines the key differences between these three pathways, focusing on custody, liquidity, and fiduciary burden.

| Method | Custody | Liquidity | Fiduciary Burden |

|---|---|---|---|

| Self-Directed Window | Third-party broker | High | Medium |

| Dedicated Menu | Plan sponsor vetted | Medium | High |

| Direct Rollover | Self-directed IRA | Variable | Low (for employer) |

Fiduciary duties and custody risks

Plan sponsors are now navigating a significantly more complex liability landscape. The Department of Labor’s proposed rule introduces a safe harbor for fiduciaries who include cryptocurrency and other alternative assets in 401(k) plans, but this protection comes with strict operational requirements. Sponsors must demonstrate that they have performed due diligence comparable to that required for traditional assets, shifting the burden of proof squarely onto the plan administrator.

Custody solutions are the primary point of failure in this new regulatory environment. Unlike traditional securities held by major custodians, crypto assets require specialized cold storage and multi-signature protocols. The DOL expects plan sponsors to verify that their chosen custodians have robust insurance coverage, clear audit trails, and segregation of assets. Failure to validate these controls can result in personal liability for fiduciaries, even if the asset itself performs well.

Valuation transparency adds another layer of compliance burden. Crypto markets operate 24/7, creating challenges for accurate daily pricing and net asset value calculations. Sponsors must ensure their record-keepers can handle real-time price feeds from reputable exchanges and reconcile discrepancies immediately. Without a standardized valuation framework, errors can accumulate, triggering ERISA violations.

The technical reality of market volatility cannot be ignored when assessing these risks. Fiduciaries must evaluate whether the potential for high returns justifies the exposure to extreme price swings, especially given the lack of historical data for digital assets in retirement portfolios.

The combination of custody gaps and valuation ambiguity means that simply offering crypto is no longer enough. Plan sponsors must build a comprehensive compliance infrastructure that includes regular third-party audits and clear participant disclosures. Ignoring these mechanical requirements invites regulatory scrutiny and potential lawsuits from participants who suffer losses due to operational failures rather than market movements.

Market Impact and Asset Allocation

The Department of Labor’s 2026 guidance shifts crypto from a speculative fringe asset to a permissible fiduciary option, potentially unlocking trillions in dormant 401(k) capital. While U.S. retirement plans hold vast sums, the actual inflow into digital assets will likely be modest and highly selective. Even a 1% allocation shift across major plans represents billions in new liquidity, yet it remains a fraction of the total retirement market.

Capital Inflow Dynamics

Fiduciaries are bound by the prudent investor rule, meaning they cannot allocate retirement funds to volatile assets without rigorous justification. This regulatory constraint acts as a natural brake on rapid adoption. Most plan sponsors will likely start with a 1% to 2% cap, focusing on established assets like Bitcoin rather than altcoins. This cautious approach stabilizes the market against sudden, large-scale dumps while providing a steady baseline of institutional demand.

Risk Management and Volatility

Crypto’s historical volatility poses a direct challenge to retirement accounts designed for long-term stability. The new rules require plan providers to offer crypto options as separate, voluntary investment choices rather than default fund allocations. This separation ensures that conservative investors are not exposed to digital asset risk. Plan sponsors must also implement robust custodial solutions to protect assets, a requirement that filters out smaller, less secure crypto platforms.

Broader Market Stability

The entry of retirement capital introduces a new layer of market depth. Unlike speculative traders who chase short-term gains, retirement accounts are long-term hold vehicles. This structural change reduces the impact of daily price swings on the broader market. As more institutions adopt crypto-friendly 401(k) platforms, the asset class gradually aligns with traditional financial infrastructure, reducing systemic risk over time.

Compliance checklist for 2026

Plan sponsors must treat the Department of Labor's proposed safe harbor as a rigorous compliance framework rather than a simple permission slip. The new rules shift the burden of proof onto fiduciaries to demonstrate that cryptocurrency options are prudent investments for retirement participants.

Document every step of the evaluation process. The DOL requires evidence that you selected crypto options based on objective criteria, such as long-term performance and liquidity, rather than speculative trends. Failure to maintain this record defeats the safe harbor.

Not all plan service providers can handle digital assets. Verify that your custodian has robust cybersecurity protocols and insurance coverage for digital holdings. The administrator must be able to handle the unique settlement and valuation cycles of crypto markets.

Set conservative caps on how much participant funds can be allocated to cryptocurrency. The DOL expects fiduciaries to limit exposure to high-volatility assets to protect retirement savings. Establish clear guidelines for rebalancing and withdrawal procedures.

Revise your plan summary description and participant disclosures to clearly explain the risks associated with crypto investments. Ensure that all legal documents comply with the new proposed 2026 regulations to avoid future liability.

This process requires careful attention to regulatory details. Plan sponsors should consult with legal counsel to ensure all actions align with the latest DOL guidance.

Common questions about 2026 rules

The 2026 Department of Labor (DOL) rule does not mandate cryptocurrency in retirement plans, nor does it automatically enable it. Instead, it removes prior barriers that allowed plan sponsors to offer alternative assets, including Bitcoin and Ethereum, if they deem them prudent investments for specific participants.

Is crypto coming to a 401k?

Crypto is not universally available in 401(k) plans. Participation depends entirely on your employer’s plan sponsor. While the DOL rule permits it, many large employers have not yet updated their investment menus. You must check with your HR department or plan administrator to see if a self-directed brokerage window or specific crypto funds are offered.

Will 2026 be a big year for crypto?

Market performance is independent of regulatory changes. While the DOL rule expands access, it does not guarantee price appreciation. Investors should view this as a structural change in availability, not a signal for market direction. Historical volatility remains high, and past performance is not indicative of future results.

Will 401k grow in 2026?

Traditional 401(k) growth depends on broader market conditions, not the inclusion of crypto. The DOL rule is a compliance framework, not an economic stimulus. Your plan’s growth will continue to rely on the performance of your selected investments, whether they are index funds, stocks, or newly permitted digital assets.

Will crypto be taxed in 2026?

Yes. The tax treatment of cryptocurrency in a 401(k) follows standard retirement account rules. Contributions are typically pre-tax (traditional) or after-tax (Roth). You do not pay taxes on crypto gains while they remain in the plan. Taxes are due upon withdrawal, based on your ordinary income tax rate at that time.

No comments yet. Be the first to share your thoughts!