Check if your plan allows crypto

Most standard employer-sponsored 401(k) plans do not include cryptocurrency. They typically restrict investment choices to a menu of mutual funds, exchange-traded funds (ETFs), and company stock. To hold Bitcoin or Ethereum, you generally need access to a self-directed brokerage window, often called a self-directed IRA or SD401(k) feature, which permits alternative assets.

The regulatory landscape for crypto in 401k 2026 is shifting, but the default remains conservative. In early 2026, the U.S. Department of Labor proposed a rule aimed at removing litigation barriers that have historically discouraged fiduciaries from offering alternative assets. This proposed rule does not mandate crypto inclusion, but it signals a potential easing of restrictions that could allow more plan sponsors to offer these options without fear of excessive liability [1].

To determine if your specific plan qualifies, you must review your official plan documents or contact your human resources department. Look for keywords such as "self-directed brokerage," "self-directed option," or "alternative investments." If your plan lacks this feature, you cannot directly purchase Bitcoin or Ethereum through your 401(k). In that case, you may need to consider a self-directed IRA or other taxable investment accounts to gain exposure to digital assets.

[1] https://www.fintechweekly.com/news/labor-department-401k-crypto-alternative-assets-rule-2026

Choose a crypto-friendly custodian

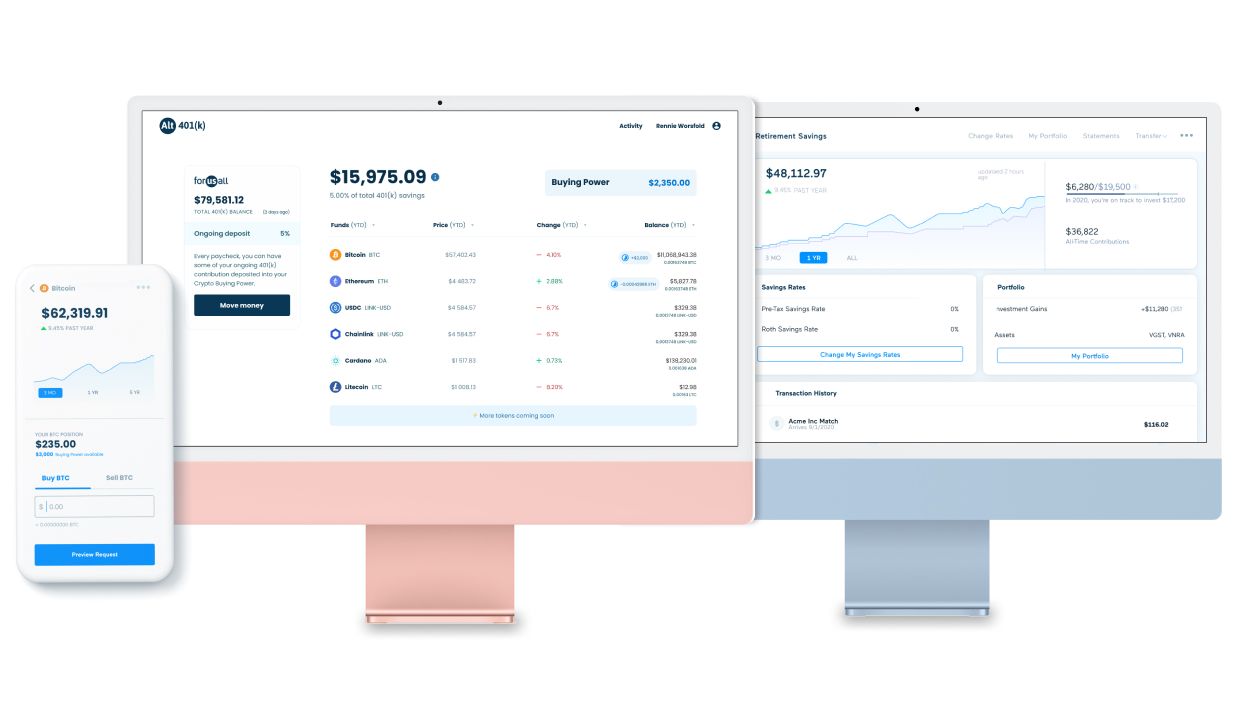

Selecting the right custodian is the first concrete step in adding Bitcoin and Ethereum to your 401(k) in 2026. Most traditional 401(k) providers do not support cryptocurrency holdings directly. You will likely need a self-directed 401(k) custodian that specializes in alternative assets.

When evaluating providers, focus on three factors: supported coins, fee structure, and setup requirements. Some custodians only allow Bitcoin and Ethereum, while others offer access to dozens of altcoins. Fees vary significantly, with some charging high annual maintenance fees and others offering zero-cost setup with low trading fees. Security is paramount; ensure the custodian uses cold storage for digital assets and offers multi-signature wallets.

The table below compares three leading self-directed 401(k) custodians that support cryptocurrency investments. Use this comparison to narrow your options before contacting providers directly.

| Custodian | Supported Coins | Fee Structure | Setup Requirements |

|---|---|---|---|

| ForUsAll | Bitcoin, Ethereum, 100+ altcoins | 0.15% trading fee, no setup fee, no minimums | Online application, employer sponsorship required |

| Bitcoin 401k | Bitcoin, Ethereum, Litecoin | Annual account fee, trading fees vary by coin | Employer plan adoption, KYC verification |

| iTrust Capital | Bitcoin, Ethereum, 15+ altcoins | $19.99 per trade, no annual fee | Self-directed IRA or Solo 401(k) account |

Once you have identified a custodian, you will need to open an account. This process typically involves completing an application, providing personal identification, and setting up your investment preferences. Some custodians require employer sponsorship, while others allow individual retirement accounts. Be prepared to verify your identity through a Know Your Customer (KYC) process, which is standard for cryptocurrency transactions.

After opening your account, you can fund it and begin purchasing Bitcoin and Ethereum. Some custodians allow direct rollovers from existing 401(k) plans, while others require you to make new contributions. Check with your custodian for specific funding instructions and any potential tax implications.

As an Amazon Associate, we may earn from qualifying purchases.

Choosing a custodian is a significant decision that affects your retirement portfolio's flexibility and security. Take your time to compare options and read the fine print. The right custodian will align with your investment goals and provide the support you need to manage cryptocurrency holdings in retirement.

Fund your self-directed account

To hold Bitcoin and Ethereum in a retirement plan, you must move existing funds into a self-directed custodian that supports crypto assets. This process typically involves rolling over money from a current employer-sponsored 401(k) or a traditional IRA. The goal is to establish a new account with a specialized provider before executing any trades.

Contact your current 401(k) plan administrator to request a distribution. Specify that you want a direct rollover, where funds are sent directly to the new self-directed custodian. Avoid an indirect rollover, where you receive the check personally, as this triggers immediate tax withholding and potential penalties.

Select a self-directed IRA custodian that explicitly supports cryptocurrency investments. Complete the account opening process, ensuring the account type matches your source funds (e.g., Traditional IRA for a Traditional 401(k) rollover). Verify that the custodian offers secure storage for Bitcoin and Ethereum.

Once the custodian account is active, initiate the transfer from your former employer’s plan. The funds should appear as cash in your new self-directed account. Do not invest these funds until the cash has fully cleared and is available for trading within the new platform.

Verify that the full rollover amount has been received in your self-directed account. Once confirmed, you can place orders to buy Bitcoin and Ethereum through the custodian’s trading interface. Ensure you understand any trading fees or spreads associated with crypto transactions.

This rollover process is a standard procedure for accessing alternative assets in retirement savings. By moving your funds to a self-directed structure, you gain the flexibility to invest in crypto while maintaining the tax-advantaged status of your retirement account.

Buy Bitcoin and Ethereum

Adding cryptocurrency to your 401(k) requires using a self-directed brokerage window within your retirement plan. This feature allows you to trade assets outside the standard mutual fund menu. The process is straightforward but carries higher volatility than traditional holdings, so precision matters.

Most major 401(k) providers, including Fidelity and Vanguard, offer a self-directed brokerage option. Log in to your plan and look for a "Trade" or "Invest" tab. If you do not see this option, your plan may not support crypto investments yet. Contact your plan administrator to confirm eligibility before proceeding.

Decide how much of your contribution goes to crypto. The IRS 401(k) limit for 2026 is $24,500, with an additional $7,500 catch-up for those over 50. You can allocate a portion of this total to Bitcoin and Ethereum. Be careful not to exceed your overall contribution limit, and remember that crypto trades are often funded from your existing cash balance within the plan.

Search for the ticker symbols for Bitcoin and Ethereum. Most platforms use standard tickers like BTC or ETH, or they may offer specific crypto trusts. Enter the dollar amount or number of coins you wish to purchase. Review the fees carefully; some platforms charge higher transaction fees for crypto trades than for standard index funds.

Cryptocurrency is highly volatile. Set up alerts for significant price movements. Unlike traditional stocks, crypto does not pay dividends, so your returns depend entirely on price appreciation. Regularly review your allocation to ensure it does not exceed your risk tolerance. If crypto grows to become a large portion of your portfolio, consider selling some to rebalance into safer assets.

Focus only on Bitcoin and Ethereum. These are the only two cryptocurrencies currently recognized as compliant with most 401(k) fiduciary standards. Investing in smaller altcoins introduces unnecessary regulatory risk and potential disqualification of your entire plan. Stick to the majors to keep your retirement account secure.

Avoid prohibited transaction risks

Adding Bitcoin or Ethereum to your 401(k) is not like buying crypto on an exchange. Your retirement account is a regulated trust with strict IRS rules. Violating these rules can trigger immediate taxes and severe penalties, effectively destroying the tax-advantaged status of your savings.

The primary danger is self-dealing. The IRS prohibits you from using plan assets for your personal benefit. This means you cannot lend money from your 401(k) to buy crypto for a friend, nor can you use your retirement holdings as collateral for a personal loan. Even indirect benefits, such as using a company vehicle funded by plan assets to transport crypto hardware, can be flagged as prohibited transactions.

Another common pitfall is investing in unregulated or obscure tokens. While some platforms offer a wide array of altcoins, many of these lack the regulatory oversight required for fiduciary compliance. If your plan sponsor or custodian does not explicitly approve a token, holding it may violate the plan’s terms. Stick to major assets like Bitcoin and Ethereum unless your plan document explicitly lists other approved cryptocurrencies.

To stay compliant, verify that your provider is a qualified custodian. They must hold the assets in a segregated account, not on a public exchange where you control the private keys. If you manage the keys, you likely have control over the assets, which the IRS views as a prohibited self-dealing event.

-

Verify no self-dealing: Ensure no plan assets are used for personal gain or loans.

-

Confirm no personal use: Do not use crypto holdings as collateral or for personal transactions.

-

Check approved assets: Only hold cryptocurrencies explicitly listed in your 401(k) plan document.

No comments yet. Be the first to share your thoughts!