The 2026 Regulatory Shift

Use this section to make the Crypto in 401k decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Fiduciary duty and prudence

The Department of Labor’s proposed rule changes signal a shift in how plan sponsors must evaluate volatile assets like cryptocurrency. Under ERISA, fiduciaries must act solely in the interest of participants and beneficiaries. This prudence standard requires a rigorous due diligence process that treats digital assets with the same scrutiny as traditional equities or bonds.

The burden of proof has shifted squarely onto the plan sponsor. Demonstrating that a crypto allocation serves a legitimate investment purpose—such as diversification or return enhancement—requires concrete evidence. Sponsors must document how the asset fits into the broader portfolio strategy and prove that the risks are manageable and understood.

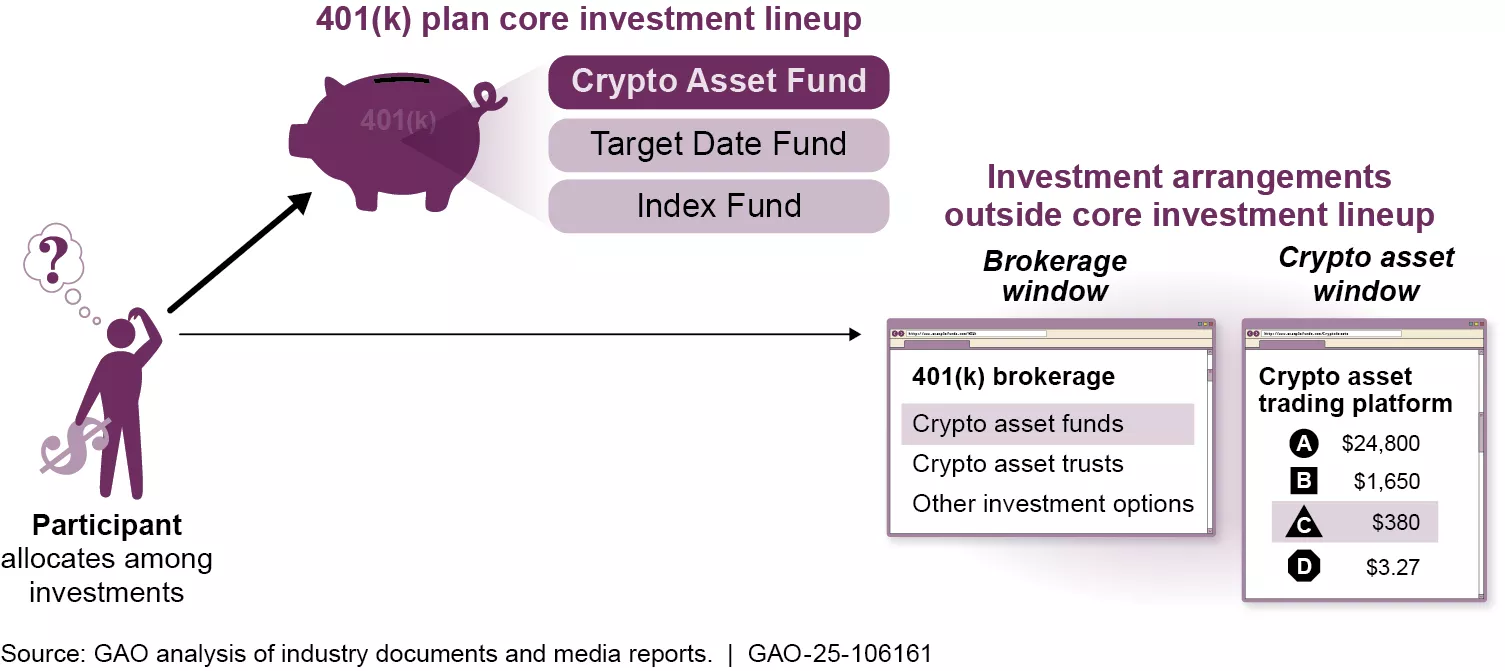

Compliance is no longer optional for those offering these options. Plan sponsors must establish clear policies for custodial security, valuation, and liquidity. Without robust safeguards, offering crypto in a 401(k) plan exposes fiduciaries to significant legal liability. The focus remains on protecting retirement savings through disciplined, well-researched investment choices.

Market Context and Volatility

The introduction of digital assets into 401(k) plans operates within a market defined by structural liquidity shifts and regulatory clarity rather than speculative hype. In 2026, the primary driver for adoption is not price appreciation alone, but the convergence of clearer fiduciary standards and expanded institutional access. As the IRS increased 401(k) contribution limits to $24,500 for 2026, the potential capital flowing into these plans has grown, creating a deeper liquidity pool for crypto assets integrated into retirement portfolios.

However, volatility remains the central risk for fiduciaries managing these accounts. Unlike traditional equities or bonds, cryptocurrency markets experience rapid, high-magnitude price swings that can erode retirement savings before they mature. The U.S. Department of Labor (DOL) emphasizes that plan sponsors must weigh this volatility against the potential for diversification benefits. The goal is not to chase short-term gains, but to manage risk within a legally compliant framework that protects participants from catastrophic loss.

The following chart illustrates Bitcoin’s price action over the past year, highlighting the extreme variance that retirement planners must account for when allocating even small percentages of a 401(k) to digital assets.

Current market conditions reflect a maturing industry. While 2025 was characterized by under-delivered price performance but over-delivered fundamental growth, 2026 presents a landscape where regulatory frameworks are solidifying. This shift suggests that while prices may remain volatile, the underlying infrastructure for holding crypto in a 401(k) is becoming more robust, reducing counterparty risk for plan participants.

Compliance Checklist for Sponsors

Plan sponsors must treat cryptocurrency as a high-risk, non-traditional asset class. Under Department of Labor (DOL) guidance, fiduciaries must demonstrate that adding crypto satisfies the "prudent expert" standard. This requires rigorous documentation of participant demand, custodial security, and fee structures before implementation.

Document the specific request. The DOL emphasizes that fiduciaries should not add options based on speculation. Conduct surveys or focus groups to confirm that a significant portion of participants actively wants crypto exposure.

Select a custodian with proven institutional-grade security. Verify that the provider uses cold storage, multi-signature wallets, and carries adequate fidelity insurance. The custodian must be able to provide clear audit trails for all transactions.

Analyze all associated costs. Crypto assets often carry higher trading fees and custody charges than traditional equities. Ensure these fees are reasonable and do not disproportionately burden participants, which could violate fiduciary duty under ERISA.

Amend the Plan Document and Summary Plan Description (SPD) to explicitly include cryptocurrency as an eligible investment option. This ensures legal clarity and protects the sponsor from claims of unauthorized discretion.

| Provider | Trading Fees | Security Model |

|---|---|---|

| ForUsAll | 0.15% | Institutional custody |

| Traditional Broker | Varies | Standard custody |

The regulatory landscape remains fluid. Sponsors should consult with legal counsel specializing in ERISA to ensure all compliance measures are current with 2026 fiduciary standards.

Participant contribution limits

The Internal Revenue Service has adjusted 401(k) contribution limits for 2026, increasing the base employee deferral amount to $24,500, up from $23,500 in the prior year. This adjustment is part of a standard cost-of-living update designed to maintain the real value of retirement savings. For participants aged 50 and older, the catch-up contribution limit remains at $8,000, allowing eligible individuals to contribute up to $32,500 annually to their employer-sponsored plans.

Solo 401(k) plans, available to self-employed individuals and business owners with no employees other than a spouse, offer significantly higher aggregate limits. For 2026, eligible participants can contribute up to $72,000 annually. If the participant is age 50 or older, the total limit rises to $80,000. These higher limits provide substantial tax-advantaged space for allocating funds into alternative assets, including cryptocurrency, within a self-directed Solo 401(k) structure.

It is critical to distinguish between traditional 401(k) plans and Solo 401(k) structures when planning crypto allocations. Traditional plans are employer-sponsored and subject to plan document restrictions that may prohibit or limit crypto investments. Solo 401(k) plans offer greater flexibility, allowing the participant to act as both employer and employee, thereby maximizing contributions and potentially accessing a broader range of investment options, provided the plan administrator permits such assets.

Participants must adhere to these limits strictly to maintain tax-qualified status. Exceeding contribution limits can result in significant tax penalties and the loss of favorable tax treatment for the plan. Consultation with a qualified tax advisor or retirement plan specialist is recommended to ensure compliance with current IRS regulations and plan-specific rules.

Common Questions on Crypto 401k

The regulatory environment surrounding cryptocurrency in retirement accounts is shifting rapidly. Understanding the specific mechanics of the Department of Labor’s proposals and the current availability of these assets is essential for fiduciaries and plan sponsors navigating 2026.

Fiduciaries must weigh these changes against strict compliance standards. The shift is not about encouraging speculation but about providing a regulated pathway for alternative assets within retirement savings structures.

No comments yet. Be the first to share your thoughts!