With Bitcoin (BTC) trading at $98,427 as of November 13,2025, and new federal regulations paving the way for cryptocurrency in retirement portfolios, investors are increasingly asking: How can I add Bitcoin to my 401(k)? Recent regulatory shifts and provider innovation have made this process more accessible than ever. Here’s a detailed, step-by-step guide to help you navigate the latest landscape and integrate Bitcoin into your retirement plan for 2025.

Bitcoin’s Place in Modern 401(k) Plans

The retirement investment landscape has shifted dramatically. In August 2025, an executive order by President Donald Trump directed agencies to revise rules around alternative assets in retirement accounts. By May 2025, the Department of Labor (DOL) rescinded its restrictive guidance on crypto in 401(k)s, now allowing fiduciaries to evaluate digital assets like Bitcoin based on their own judgment under ERISA. The Securities and Exchange Commission (SEC) has also signaled openness, provided investor education and responsible disclosure are prioritized.

This regulatory clarity has encouraged major providers like Fidelity to offer a Digital Assets Account within select 401(k) plans, making it possible for eligible participants to allocate a portion of their portfolio directly to Bitcoin. However, it’s crucial to recognize that access depends on your employer’s plan policies and provider choices.

Step-by-Step: Adding Bitcoin to Your 401(k) in 2025

How to Add Bitcoin to Your 401(k): A Visual Step-by-Step Guide (2025)

Let’s walk through the essential steps you need to follow:

1. Confirm Your 401(k) Plan Allows Bitcoin Investments

Your first move is straightforward but critical: Check with your employer or plan administrator. Not every plan offers crypto exposure yet, even among large providers like Fidelity or Charles Schwab. Ask directly if your plan includes a crypto or Digital Assets Account option for 2025. If not, inquire about future plans or potential rollovers into providers that do.

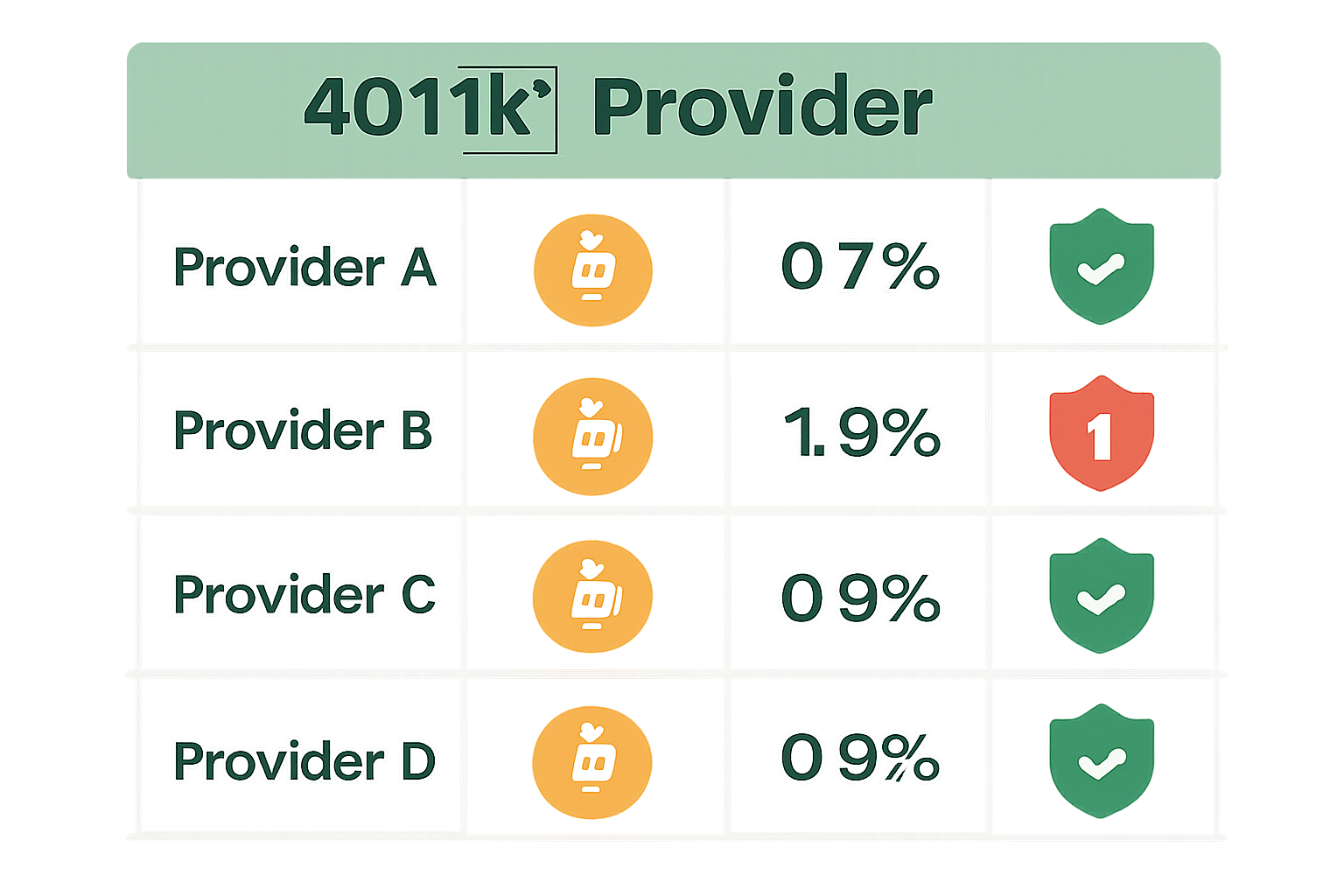

2. Review Provider Options and Fees

If you have access to a crypto-enabled plan, compare the available 401(k) bitcoin providers. Key factors include:

- Custodial security: How are digital assets stored? Cold storage solutions are best practice.

- Supported cryptocurrencies: Most plans currently offer only Bitcoin exposure, ideal for those seeking blue-chip digital asset diversification.

- Management fees: Crypto allocations often carry higher fees than traditional index funds; review these carefully before allocating funds.

- DOL compliance: Ensure the provider adheres to updated Department of Labor guidelines for crypto in retirement accounts.

This due diligence is essential, fees can erode long-term returns if not managed prudently.

Navigating Eligibility and Risk Tolerance

The next step is personal: Assess eligibility requirements and your risk tolerance. Some plans may require minimum balances or restrict maximum allocation percentages (often capped at around 5-10% of your total portfolio). More importantly, consider whether adding Bitcoin aligns with your overall retirement goals and appetite for volatility. While crypto offers non-correlation benefits relative to stocks and bonds, a point highlighted by many financial advisors, it also introduces unique risks that must be balanced within a diversified portfolio.

If you’re unsure how much exposure makes sense for you or want help interpreting your plan’s specific rules, consult with a fiduciary financial advisor familiar with digital assets in retirement planning. For more guidance on optimal allocations by age and risk profile, see our related resource: How Much Bitcoin Do You Need in Your 401(k) To Retire?

4. Allocate Funds to the Bitcoin Option

Once you’ve confirmed eligibility and selected your provider, it’s time to allocate funds to the Bitcoin investment option within your 401(k). Log in to your plan dashboard, if you’re with a provider like Fidelity, look for the “Digital Assets Account” or similar section. Follow your plan’s instructions to designate a specific percentage or dollar amount of your portfolio to Bitcoin. Many plans set minimum and maximum allocation thresholds (commonly 1-5% minimum, up to 10% maximum), so review these carefully.

Remember: Allocating even a modest portion of your retirement savings to Bitcoin can meaningfully increase diversification, but it also adds volatility. Start small if you’re new, and avoid over-concentration in any single asset class.

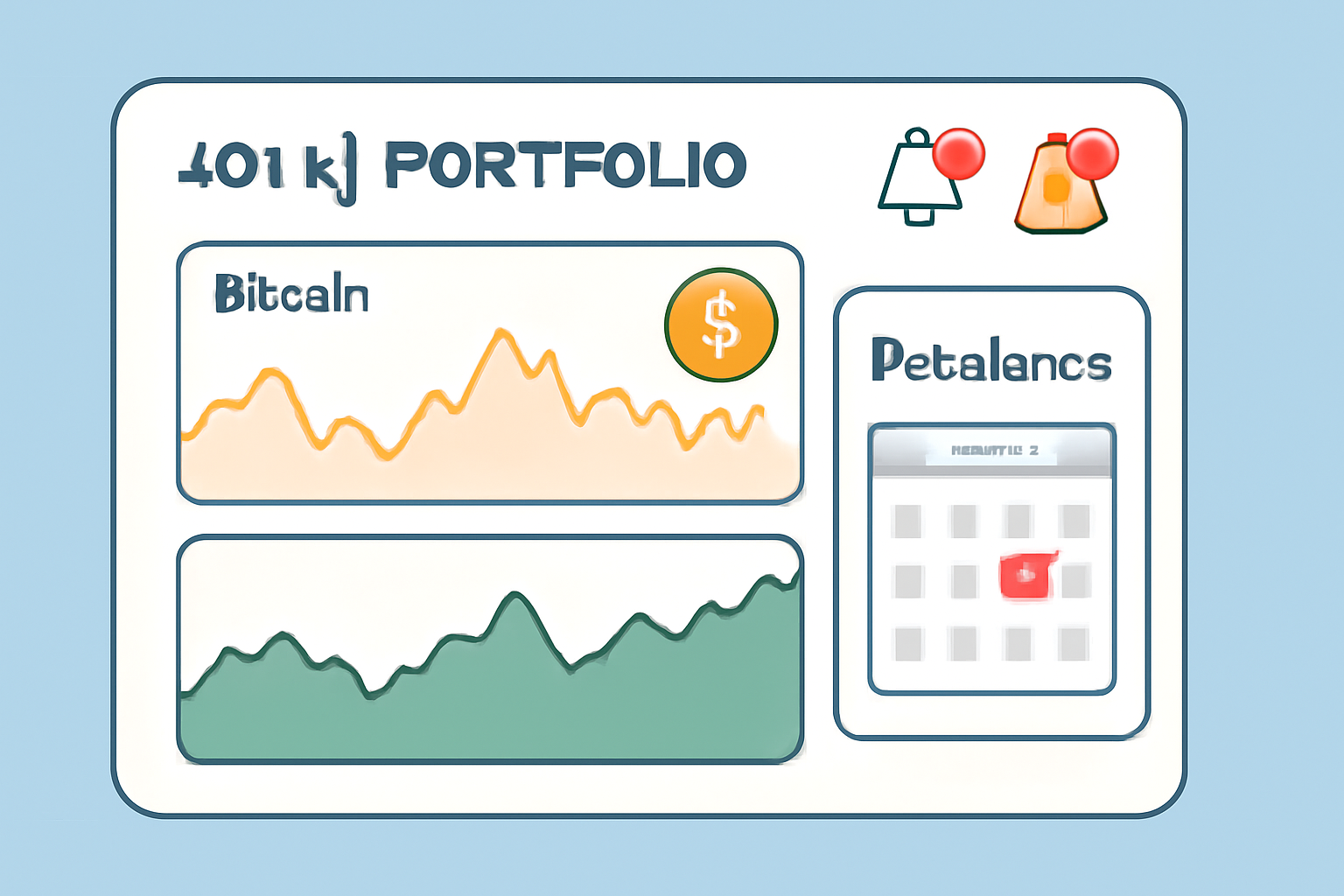

5. Monitor Performance and Rebalance Regularly

After allocation, ongoing monitoring is essential. With Bitcoin trading at $98,427 as of November 13,2025, and experiencing daily fluctuations exceeding $5,000, it’s vital to keep tabs on performance within your retirement account. Use your provider’s tools or third-party apps for real-time tracking. Regulatory changes can also impact plan rules or available options, so stay informed about Department of Labor updates and SEC guidance throughout the year.

Set a schedule (quarterly or semi-annually) to review your crypto allocation alongside other assets in your 401(k). If market movements push Bitcoin above or below your target range, rebalance accordingly by trimming gains or adding on dips, always in line with your risk tolerance and long-term strategy.

Key Considerations for Crypto Diversification in Your Retirement Plan

The ability to add Bitcoin to your 401(k) brings new opportunities, and responsibilities, for retirement investors. While regulatory barriers have eased and mainstream providers are entering the space, it’s still crucial to:

- Understand tax implications: Crypto gains within a 401(k) are tax-deferred (traditional) or tax-free (Roth), but distributions will be taxed according to plan rules.

- Avoid emotional decision-making: Crypto markets are volatile; stick with disciplined rebalancing rather than reacting impulsively to price swings.

- Document all transactions: Keep records of allocations and rebalancing actions for compliance and personal tracking purposes.

- Stay educated: Ongoing learning is essential as new products (like spot Bitcoin ETFs) may be added by providers in response to regulatory evolution.

If you want more detailed walkthroughs on building a crypto retirement plan, explore our comprehensive guides covering everything from initial setup through advanced portfolio management strategies.

The Bottom Line: Is Adding Bitcoin Right for Your 401(k)?

The path toward integrating digital assets into retirement accounts is clearer than ever in late 2025, but not universal. Confirming access through your employer’s plan administrator remains step one; from there, diligent provider research and honest self-assessment of risk tolerance are vital before making an allocation. Once invested, regular monitoring ensures that crypto exposure remains aligned with long-term goals despite inevitable market volatility.

This approach empowers forward-thinking investors seeking true diversification within their retirement portfolios, while staying compliant with evolving regulations. As always: Plan smart, invest smarter.

No comments yet. Be the first to share your thoughts!